Report Overview

Get more information about how the increase in high-end special purpose wipes sales are boosting value gains.

This Freedonia industry study analyzes the $443 million US household care wipes industry. It presents historical demand data (2011, 2016 and 2021) and forecasts (2026 and 2031) by application (general purpose, floor care, other), and type (wet, dry). Floor care wipes are broken into electrostatic and wet wipes. Other household care wipes are broken into dusting & polishing wipes and glass wipes. The study also evaluates company market share and competitive analysis on industry competitors including Nice-Pak, Proctor & Gamble, Clorox, Rockline, and Kimberly-Clark.

Featuring 23 tables and 13 figures – available in Excel and Powerpoint! Learn More

Demand for household care wipes is expected to grow just 1.1% percent per year (off of a high 2021 base) to $448 million in 2026, limited by a decline in unit sales. Consumer use of wipes will continue to normalize following a pandemic-related spike in 2020. However, growth in market value will be supported by:

- growing demand for sustainably sourced materials, which will support higher pricing and greater market value

- value-added features, such as natural scents from essential oils and custom scent blends

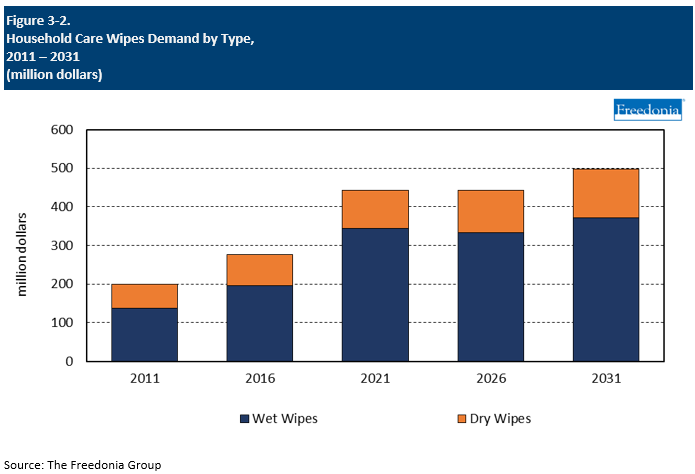

Wet Wipes Continue to Dominate but Dry Wipes Regain Market Share

Wet wipes have historically been more widely used in household settings due to the convenience they offer over traditional towels and spray bottles. This trend will continue, though dry wipes will gain some market share due to strong demand for electrostatic floor care wipes as the installation of hard surface flooring in homes continues to rise in popularity. Wet wipes will still be heavily favored for surface disinfection, glass cleaning, and general purpose cleaning.

Prices Stabilize after Turbulent 2020-2022

The average price of household care wipes dipped during the pandemic. This was attributable to a shift in consumer habits, as buyers began to use less expensive general cleaning wipes instead of specialty products. This was exacerbated by an influx of lower-cost private label brands that came on the market to help meet the sharp increase in demand, and then remained on shelves after the immediate wave subsided. Consequently, retailers were left with a glut of commodity disinfectant wipes.

Following an inflation-related spike in 2022, prices will remain elevated as consumers revert back to pre-pandemic buying habits that include reduced use of less expensive private label general purpose cleaning wipes and greater use of more specialized household care wipes. These prices will also be sustained by continued innovation in product formulations that incorporate higher value substrates and additives.

Demand to Remain Well Above Pre-Pandemic Levels

Growth for household care wipes will be moderate as consumers adapt and rethink their cleaning habits, in many cases (especially with surface disinfection) returning to habits that more closely resemble pre-pandemic routines. However, demand will remain well above pre-pandemic levels due to new habits that became established during the pandemic. In addition, the surge in demand during the initial phase of the pandemic expanded the base of wipes users, making a greater number of consumers more amenable to products that provide both convenience and the ability to reduce cross-contamination for house cleaning tasks.

Demand by Type

Wet vs. Dry

Household care wipes demand is forecast to remain flat at $443 million in 2026. A decline in unit terms, the result of consumer usage of wipes normalizing following sharp increases at the onset of the pandemic, will be offset by greater use of higher value wipes.

Household care wipes come in both wet and dry formulations, with the former accounting for 78% of the market. While wet wipes still dominate this market, dry household care wipes are expected to gain share. This is partially a result of increased use of floor care wipes which have high average prices and will boost value gains.

Pricing Trends

Prices for household care wipes dropped in 2020 and remained lower in 2021 due to a shift in consumer buying habits, as consumers began to favor lower-priced priced general purpose cleaning wipes. This was aided in part by less expensive private label brands having to fill the sharp increase in demand and remaining on shelves after the immediate demand subsided, causing retailers to be left with a glut of surface disinfectant wipes.

However, average prices will rebound due to a shift in product preference, as consumers revert back to pre-pandemic buying habits, which include reduced use of less expensive private label general purpose cleaning wipes. These prices will be sustained by increased demand for high-end special purpose cleaning wipes, such as dusting and polishing wipes.

Raw Materials

At their most basic, wipes are substrates (e.g., airlaid, spunlaced, composites, and paper) that may or may not be saturated with chemicals (e.g., emollients and surfactants). The materials used to create wipes often include nonwovens, which themselves are composed of fibers from both natural and synthetic sources, such as plastic. Material composition for wipes continues to see innovation of better performing products.

Additionally, the raw materials used by converters for their end-use products can be influenced by:

- costs further upstream, such as for plastic resin or fossil fuels

- the environmental profiles of the ingredients employed

- shortages of available materials due to high demand or delays in the supply chain

Wipes Regulations

Wipes that contain a wide range of chemical substances are subject to regulation by the EPA. The laws regulating wipes containing these chemicals include the FPLA and the Lautenberg Chemical Safety Act (previously known as the Toxic Substances Control Act). The FPLA gives the Federal Trade Commission authority to monitor the labeling and packaging of products such as nondisinfectant general purpose cleaning wipes and floor care wipes, just as it gives the FDA authority over cosmetic and therapeutic products.

Many industries and establishments produce solid or hazardous waste, the disposal of which is regulated by the EPA under the authority of the Resource Conservation and Recovery Act (RCRA). Manufacturing applications are especially likely to require such regulation due to the various byproducts of manufacturing processes.