Report Overview

Featuring 26 tables and 24 figures – now available in Excel and Powerpoint! Learn More

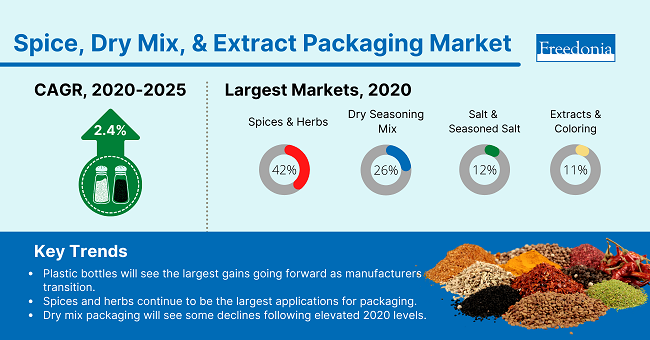

Packaging for spices, dry mixes, and extracts is forecast to grow 2.4% per year to $1.1 billion in 2025 off of a high 2020 base, when sales of these products spiked as a result of a shift in eating habits at the onset of the COVID-19 pandemic. Growth will be supported by the popularity and variety of spices and other seasoning products offered by retailers, as well as the increasing usage of premium packaging for product differentiation purposes.

Packaging for spices, dry mixes, and extracts is forecast to grow 2.4% per year to $1.1 billion in 2025 off of a high 2020 base, when sales of these products spiked as a result of a shift in eating habits at the onset of the COVID-19 pandemic. Growth will be supported by the popularity and variety of spices and other seasoning products offered by retailers, as well as the increasing usage of premium packaging for product differentiation purposes.

Demand by Packaging Format (Rigid vs. Flexible)

Packaging for spices, dry mixes, and extracts is dominated by rigid packaging, although this varies greatly in the individual segments. In many other food categories, rigid packaging has been losing share to flexible due to the latter’s lighter weight and amenability to source reduction. However, due to the ease-of-use of rigid containers – especially important when working in the kitchen – salt, spices and seasonings remains one of the few food categories where flexible packaging will lose slight share to rigid.

Flexible packaging such as pouches and bags are still used to some extent with these products, usually for single-serving items – foodservice salt and pepper packets or recipe mixes in side-seal pouches – or for commercial sized foodservice products (bags and liners). Bags and pouches are also used for refill applications (currently almost all by specialty online spice retailers) and this could be a growth opportunity for flexible packaging if trends toward refills take hold as they have in some non-food sectors.

Materials Trends

Demand by Material

Plastic is the most common material used in the packaging of spices, dry mixes, and extracts due to its prevalence in bottles, pouches, and bags. Plastic bottles benefit from their enhanced performance and lower cost compared to glass and paperboard alternatives, and they will continue to take market share from containers based on other materials going forward. This trend is evident in Morton Salt’s recent move to replace its iconic paper canisters with plastic bottles.

Despite competition from plastics, paper and paperboard packaging will continue to see use where paper pouches or folding cartons are prevalent; glass will continue to be used with specialty spices due to its premium image.

Other materials, mainly metal, will continue to lose share going forward as manufacturers switch to other, less costly options.

Factors Impacting Packaging Demand

Spice & Seasoning Shipment Trends

Demand for packaging used with spices, dry mixes, and extracts is directly influenced by the demand and production of the products themselves, as well as their target end users. Both the overall levels of spice production and the fluctuating shares of different types of spices, seasonings and mixes – which may require different amounts and types of packaging – have an impact on packaging demand.

US shipments of spices, dry mix, and extracts will increase nearly 1.0% annually to $9.7 billion in 2025, with advances limited by coming off a high 2020 base. However, usage will continue to be supported by an expanding variety of spices, mixes, and seasoning products, including international spices, unique seasoning mixes, and premium salts.

Packaging will benefit as products like spices and herbs increase their share of the overall product mix, as these tend to be the most packaging intensive.

The scope of this report includes packaging for spices, herbs, seasonings, dry mixes, salt, extracts, and food coloring. These items are generally sold in a dedicated section of retail store but are also used by foodservice establishments.

Specific applications covered in this report include:

- dip and dressing mixes, including mixes to make salad dressings and savory dips

- dry seasoning mixes, which are blends of spices, herbs and other food products that are used to prepare a specific dish, such as tacos

- flavoring extracts and food colors, including emulsions, liquid flavors, pastes, and gels

- salt and seasoned salt (a blend that is predominantly salt with other added spices or seasonings), including salt substitutes

- other dry mixes, including:

- sauce mixes, used to make cheese sauces, ethnic sauces, gravy and other savory sauces

- spices and herbs, such as black pepper, turmeric, thyme, and spice blends

Excluded from this study are a variety of products including:

- synthetic food colors

- bulk salt, dry mixes, extracts, and spices used in food manufacturing

- salt for other consumer, agricultural, or industrial applications

- dry mixes used to make sweet foods such as cakes, cookies, frosting, or pudding

- corrugated boxes and protective packaging used specifically for shipping purposes as opposed to product packaging

Specific packaging products used for spices, dry mixes, and extracts are:

- bottles and jars

- pouches and bags

- boxes and cartons

- canisters

- other packaging such as tubs and pails

Historical data (2010, 2015, and 2020) and forecasts for 2025 and 2030 are presented for demand for spice packaging by value in current dollars (including inflation); demand data by market is presented in current dollars. “Demand” (or sales) is defined as all shipments from US plants, plus imports minus exports.

Demand for packaging used with spices, dry mixes, and extracts is projected to grow 2.4% per year to $1.1 billion in 2025 from a high base in 2020, when the market for these products was boosted by the pandemic. While growth will be below historical norms, the market will benefit from:

- the increasing popularity and variety of spices offered by retailers

- rising use of premium packaging for product differentiation purposes

- a lingering higher level of interest in home cooking and baking

Plastic Bottles to Experience the Largest Gains as Manufacturers Transition

McCormick and Morton – the biggest spice and salt suppliers, respectively – have begun transitioning away from metal and paperboard canisters toward plastic bottles, which are lighter and easier to recycle:

- In Morton’s case, the bottles feature a plethora of convenience features and are designed to have increased shelf appeal. They are also transparent, allowing consumers to see the salt inside and gauge how much is left.

- McCormick has used plastic canisters in many of its products for some time and has moved away from metal for iconic brands like Old Bay, in part to increase sustainability of these high-volume products. The company has also pledged to decrease the environmental impact of its plastic packaging by using more recycled content in its creation and ensuring that the containers can be reused or recycled by 2025.

Spice & Herb Packaging Continues To Be the Largest Market

Spices and herbs are intensive users of packaging, as containers tend to be smaller and use higher value features than other seasonings. In addition, an increasing variety of ethnic and specialty spices continues to become available. Spices and herbs are the only category to make significant use of glass packaging, which imparts the perception of quality and freshness and is commonly used with premium spices and herbs.

Demand for Dry Seasoning Mixes Packaging to Face Declines from Elevated Level in 2020

While all spice and seasoning categories saw increased demand in 2020 as consumers cooked and baked at home more frequently, dry mixes experienced an especially high bounce in part because they are premeasured and easy-to-use in the kitchen. This was especially important for consumers with little or no cooking experience who began cooking more during the first year of the pandemic. While sales of dry mixes are expected to return more sustainable levels, demand is expected to remain above historical levels. Even as consumers begin to spend more time out of the home, those who became accustomed to using dry seasoning mixes are likely to continue to do so more often.