Report Overview

Featuring 28 tables and 59 figures – available in Excel and Powerpoint! Learn More

This report includes data from 2012-2032 in 5 year intervals and tables featuring year-by-year data for 2018-2026.

This study examines the US market for molded fiber foodservice disposables, defined as rigid packaging formed from fibrous materials used by foodservice locations to serve and  package food, and meant to be disposed of. Serviceware – such as dinnerware, trays, and beverage carriers – is also covered. Historical data are provided for 2012, 2017, and 2022, with forecasts through 2032 in current US dollars and in units. Annual data is provided for 2018-2026. Also provided is an analysis of key industry players.

package food, and meant to be disposed of. Serviceware – such as dinnerware, trays, and beverage carriers – is also covered. Historical data are provided for 2012, 2017, and 2022, with forecasts through 2032 in current US dollars and in units. Annual data is provided for 2018-2026. Also provided is an analysis of key industry players.

The US market for molded fiber foodservice disposables continues to see strong growth attributable to an increased focus on sustainability initiatives, technological improvements, and longer-running market trends; these factors are combining to increase market size and breadth.

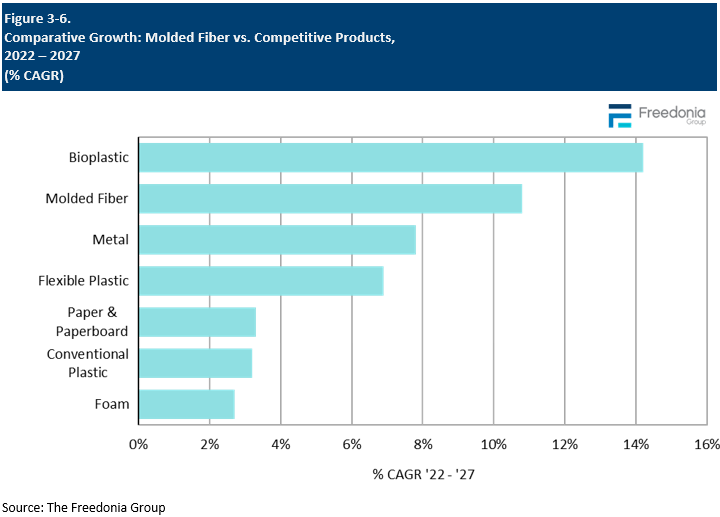

US demand for molded fiber foodservice disposables is forecast to increase 11% per year to $1.8 billion in 2027, with real growth of 11% annually to 17.8 billion units. Gains will be supported by multiple factors:

- Molded fiber will continue to benefit from perceptions of it as sustainable, recyclable, compostable, biodegradable, and from the fact that it is increasingly made from agricultural waste.

- Developments in coatings and additives will increase the number of applications for molded fiber, including high-temperature and oily products.

- Advances in manufacturing and tooling processes will continue to lower the cost of molded fiber production, especially for those sourced from alternative fibers.

Molded Fiber Taking Share from Conventional Plastic-Based Foodservice Packaging

Owing to its favorable sustainability profile and increasing cost competitiveness, molded fiber is expected to continue taking share from conventional plastic and foam iterations of products like clamshells, two-piece containers, cups, and dinnerware. Molded fiber is compostable and biodegradable in addition to being recyclable, and it is increasingly being made of nonwood fibers that enhance its sustainability profile.

Improvements in Coatings and Additives to Further Boost Molded Fiber Penetration

Historically, molded fiber did not see much use in the foodservice industry apart from a few specific products (like beverage carriers). One of the biggest deterrents was its poor moisture and heat resistance, which prevented it from being used with very hot or oily food and beverages. This issue was initially addressed through the use of PFAS-based coatings, but concerns about the health risks associated with such chemicals have only grown. In response, molded fiber packaging manufacturers have invested in less problematic fluorochemical-free products that maintain compostability and allow molded fiber to be used with a wider variety of foodservice dishes.

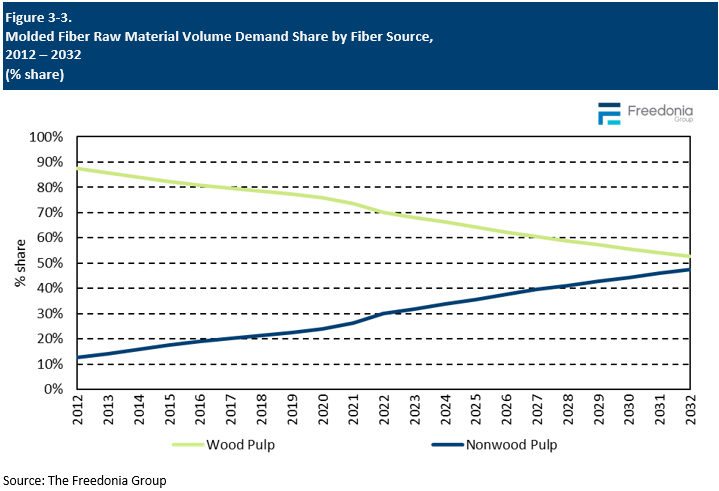

Nonwood Fibers Expected to See Especially Strong Growth

Molded wood pulp products are expected to see strong growth, but products sourced from alternative fibers – including sugarcane, wheat straw, bamboo, and various grasses – have the largest projected gains due their superior renewability, perceived sustainability, improved aesthetics, and increasing cost competitiveness. These materials also offer unique features. Wheat straw, for example, is available in a darker shade than other materials.

Historical Market Trends

At its broadest level, demand for single-use molded fiber foodservice products is driven by trends in foodservice revenue, which is an indicator of the number of meals eaten away from home and the amount spent on those meals. Growth in foodservice activity in turn is dependent on several macroeconomic and demographic factors including:

- Trends in food consumption and the mix of food eaten at home versus away from home

- The health of the overall economy and levels of disposable income, which impact the ability of consumers to spend on more expensive restaurant meals (compared to home cooking)

- Changes in the population mix, especially in terms of age cohorts (such as young adults) that are likely to eat out more often

- Trends in consumer spending, including spending on travel and entertainment, which impact foodservice sales at hotels and sports and recreation venues

- Student enrollment levels and trends in school lunch programs

Beyond these basic macroeconomic indicators, other factors that can impact the foodservice industry and demand for disposable products include:

- the mix of restaurants that are limited versus full-service, as limited-service restaurants use a higher level and broader mix of disposables

- the share of total restaurant orders that are provided via drive-thru, curbside pickup, carryout, or delivery services

- the size and diversity of restaurant menus, as specific disposables are often used with specific menu items

- social factors such as health concerns, which not only influence the amount consumers eat out but the type of foods they purchase

- sustainability initiatives, which impact the overall level of disposables used as well as the types of products and materials used

- regulations, especially restrictions on specific materials or types of disposables

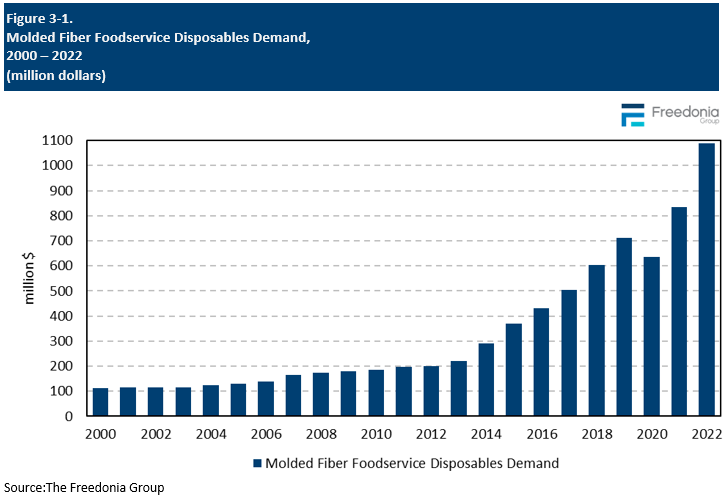

Prior to the pandemic, molded fiber disposables had experienced healthy, above average growth owing to the increasing importance of sustainability among foodservice operators. Use of molded fiber disposables dipped somewhat during 2020 as foodservice sales declined and foodservice operators increasingly focused on cutting costs and adapting to changing consumer behavior rather than maintaining a sustainable image.

However, molded fiber disposable usage recovered in 2021 and 2022 as consumers returned to eating out more often and restaurants were able to focus again on reaching sustainability targets. Molded fiber disposable usage also benefited from an increase in takeout and delivery services during and following the pandemic, as these are more packaging intensive operations and often use two-piece containers or clamshells, two of the largest molded fiber disposable product categories.

Raw Material Trends

Molded fiber has historically been produced in the US using recycled paperboard and/or newsprint as the fiber source. However, other plant-based fibers – including those from sugarcane, bamboo, wheat straw, and other agricultural byproducts – are also increasingly used to make molded fiber. All these materials are recyclable and biodegradable, and they are compostable where appropriate facilities are available.

Demand for molded fiber foodservice disposables is forecast to increase 11% per year to $1.8 billion in 2027, with real growth of 11% annually to 17.8 billion units, driven by the great sustainability profile of molded fiber. Advances will be especially strong for molded fiber products sourced from non-wood pulp which offer an even stronger image of sustainability.

Though molded wood pulp is still commonly used in the production of mature molded fiber foodservice products such as cafeteria trays and beverage carriers, more recently introduced products – such as dinnerware, cups, clamshells, and two-piece containers – are increasingly sourced from alternative fiber sources or contain mixes of wood pulp and alternative fibers. These alternative fibers potentially offer an even more sustainable image due to the growing popularity of the “No Tree” movement and are becoming increasingly cost-competitive with molded wood pulp products.

Pricing Trends

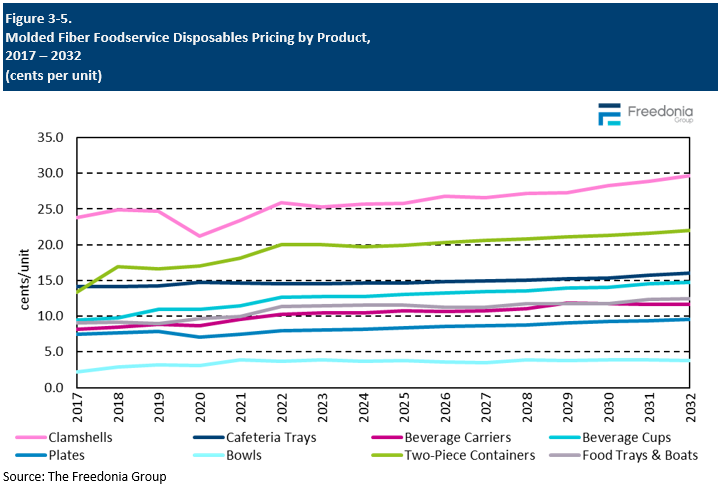

Prices for molded fiber foodservice disposables are forecast to remain flat through 2027 – coming off a high base in 2022 following inflationary pressures – reflecting some diverging trends:

- Increased focus on performance of molded fiber products to allow the material to be used with hot and oily foods will increase average price.

- However, that will be offset by advancements in manufacturing and tooling processes, which will decrease the price of production, particularly for nonwood fibers.

In general, prices for molded fiber products are determined by the following factors:

- raw material availability and costs

- labor costs

- shipping and transportation costs

- supply and demand balances

- customization, design, and printing costs

Unlike plastic products, molded fiber exhibits relative price stability, as the material is not influenced by swings in the oil industry or resin prices. Average prices for molded fiber products are instead largely affected by changes in the costs for such raw materials as post-consumer paper products and agricultural waste – materials that are less prone to dramatic price fluctuations.

Molded fiber prices are also determined by product type and manufacturing requirements (e.g., the degree of complexity, customization, and tooling necessary). While manufacturers are working to lower prices and make molded fiber more price competitive with other materials, advances to improve the quality and range of applications for molded fiber packaging are increasing average product prices.

Competitive Products

Molded fiber primarily competes with the following materials:

- EPS – used in the manufacturing of clamshells, plates, bowls, cups, and trays

- rigid polyethylene terephthalate (PET) – used in the manufacturing of clamshells, cups, and lids

- paperboard – used in the manufacturing of plates, bowls, clamshells, trays, and cups

In many cases, these materials are less costly than molded fiber, and may perform better in certain applications (such as where high strength or moisture barriers are required). EPS sees significant use in the foodservice industry compared to other markets due to its low cost and good insulation properties, especially important for the packaging of hot foods. Nevertheless, molded fiber packaging offers key advantages over each of the above materials that promote its use.

Molded fiber also competes with other materials poised as sustainable alternatives to traditional packaging – such as bioplastics – to a limited extent, particularly in replacing traditional rigid plastics. Bioplastics are better suited for rigid plastic applications for which visibility is especially important, such as cups for specialty drinks, as well as lids for two-piece containers and beverage cups.