Report Overview

Strong Interest in Pet Health and Wellness Continues to Support Demand for Pet Medications

While consumers remain highly focused on products that support preventive care and common health concerns, many are trimming discretionary spending due to economic pressures, creating headwinds for the category. As a result, the market is transitioning from pandemic-era surge growth to a steadier pace in the years ahead.

Key Themes Covered in this Report:

- Veterinary channel sales make up the bulk of the pet medications market

- Marketers and retailers must position pet medications as necessities, not “nice-to-have” products

- Cat-specific medications are a key area of opportunity

Pet Medications Growth Impacted by Vet Usage, Pet Population

The US pet medications market is facing headwinds from all sides, with economically strained pet owners, a challenged veterinary sector, shifts in the pet population, and omnimarket competition all contributing to recent changes in the market. That said, opportunities remain. Pet health and wellness remain a top priority for consumers, and strong owner commitment to maintaining pet health, combined with continued innovation in patented prescription therapies, is helping sustain the market and prevent broader sales erosion.

Packaged Facts estimates that retail sales of pet medications approached $13 billion in 2025, with market growth slowing to 3.1% in 2024 and 1.9% in 2025. Although inflationary pressures have eased across many consumer markets, pet medication manufacturers and marketers have continued to implement price increases into 2026, meaning that much of the category’s recent growth reflects higher prices rather than expanding sales volume. Marketers continue to strategize around growing competition from lower-cost generic alternatives entering the market after patent expirations.

Veterinary clinics remain the dominant distribution channel, accounting for an estimated 70% of pet medication sales, yet the veterinary sector itself is under increasing pressure. Veterinary service inflation, affordability concerns, and macroeconomic uncertainty have contributed to declining veterinary usage rates. At the same time, online retailers and other non-veterinary channels continue to gain share, intensifying competitive pressure on traditional veterinary sales.

Economic strain is visible in pet owner attitudes and purchasing behavior. Packaged Facts 2026 Surveys of Pet Owners reveal growing concern over the rising costs of pet food, veterinary care, and medications, with nearly three-quarters of pet owners agreeing that prescription pet medications cost too much. More than half worry about their ability to afford pet healthcare, while many report that broader pet care expenses are limiting medication purchases. These affordability challenges are also influencing pet ownership trends, particularly among dog owners. Packaged Facts estimates that the number of US households owning dogs declined by nearly three million between 2021 and 2025, a significant development given dogs’ outsized role in medication sales. Conversely, cat ownership has risen moderately, creating opportunities for marketers to expand focus on feline health products.

This Packaged Facts report delivers comprehensive analysis of the US pet medications market, including historical market performance from 2020 through 2025 and forecasts through 2030. The study examines pet medication sales by pet type (dogs and cats), distribution channel (veterinary clinics, online retailers, and brick-and-mortar retail), and product segment, providing in-depth coverage of both prescription pet medications and over-the-counter (OTC) pet healthcare products. Key product categories analyzed include parasiticides (flea and tick treatments, heartworm preventives) as well as coverage of other companion animal medications. The report offers detailed competitive intelligence of leading pet pharmaceutical and animal health companies shaping the US pet meds industry. The report also investigates evolving retail channel trends across veterinary practices, pet specialty retailers, mass-market outlets, e-commerce platforms, and online pet pharmacies, with special emphasis on the expanding role of digital commerce in pet medication purchasing and the shifting relationship between veterinary and retail distribution.

Consumer insights are derived primarily from Packaged Facts’ proprietary January 2026 and February 2026 Surveys of Pet Owners. Survey findings provide analysis of purchase behavior, medication usage rates, preferred retail channels, demographic segmentation, and psychographic trends, offering valuable insight into pet owner attitudes toward pet health, veterinary care, affordability, and spending on pet medications and wellness products.

Pet Medications in the US, 10th Edition Report Details

Details about the Pet Medications in the US, 10th Edition Report

| Current Total Market Size |

$13 billion in 2025 |

| Forecast Total Market Growth Rate |

2.4% CAGR for 2025-2030 |

| Historical Period |

2020-2025 |

| Forecast Period |

2026-2030 |

| Regions |

United States |

| Products |

Dog and cat medications |

| Markets |

Pet medications |

| Point Where Data is Measured |

Veterinary and retail sales |

Leading Companies Driving Trends in the Pet Medications Market

Leading Companies Driving Trends in the Pet Medication.

| Boehringer Ingelheim |

Central Garden & Pet |

| Ceva Animal Health |

Elanco |

| Hartz Mountain Corp. |

Merck Animal Health |

| Pet IQ |

Vetoquinol |

| Virbac |

Zoetis |

Pet Health and Wellness Drives Market Growth

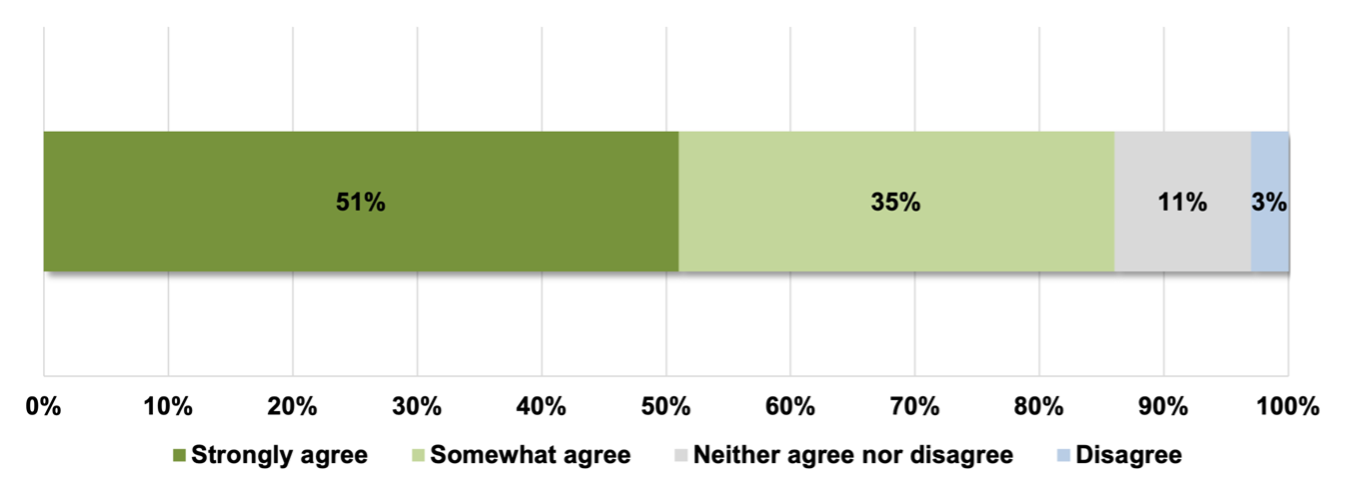

Rising healthcare awareness among US pet owners continues to support demand in the evolving pet medications market, even as economic pressures reshape purchasing behavior. According to Packaged Facts research, pet owners remain deeply committed to maintaining their pets’ health and wellness, creating ongoing opportunities across prescription pet medications, over-the-counter pet healthcare products, and preventive treatments such as flea, tick, and heartworm medications. Packaged Facts survey data show that 86% of pet owners actively monitor their pet’s health, while 72% seek products that improve overall pet wellness and quality of life.

In addition, more than half of pet owners report paying closer attention to their pets’ health than in previous years, reinforcing the growing “humanization of pets” trend driving spending across the companion animal healthcare market. This heightened focus on preventive care and wellness continues to support demand for veterinary pharmaceuticals, parasiticides, dermatology products, and pain management solutions for both dogs and cats.

At the same time, the US pet medications market is undergoing significant structural change. Veterinary clinics remain the leading distribution channel for pet medications, but online pet pharmacies and e-commerce retailers continue to gain share as consumers increasingly seek convenience, price transparency, and lower-cost alternatives. The expanding availability of generic pet medications is also reshaping competition, particularly in flea and tick prevention and other high-volume categories.

Economic pressures, however, are influencing pet owner spending priorities. Rising costs for veterinary care, pet food, and prescription medications have increased affordability concerns among consumers, leading many households to reassess pet healthcare spending. Despite these challenges, most pet owners continue to prioritize their pets’ well-being, with a large majority indicating they would cut back on personal expenses before compromising their pets’ health. Changing pet ownership trends are also influencing the future of the market. While dog ownership levels have softened in recent years, cat ownership has experienced moderate growth, creating new opportunities for pet medication manufacturers and marketers targeting feline health products. As pet owners become increasingly proactive about monitoring pet health, the demand for innovative, accessible, and value-oriented pet healthcare solutions is expected to remain a key driver of growth in the US pet medications industry through 2030.

Pet Medications in the US, 10th Edition Report Scope

Pet Medications in the US, 10th Edition, examines the US market for medications for domesticated dogs and cats, with a focus on products purchased directly by consumers. These include both prescription and over-the-counter (also called OTC or retail) medications. The primary focus of this report is on the core types of antiparasitics/parasiticides – heartworm preventatives, flea/tick preventatives, and heartworm/flea combo products, and other dewormers. Also covered are market-shaping developments in other areas, including anxiety, pain management, cancer, cognitive dysfunction, and obesity/diabetes.