Report Overview

Trends in Solar Energy Market Continuing to Fuel Flat Glass Demand Growth

The solar energy market will remain the largest driver of flat glass demand growth through 2030. However, geographic opportunities are evolving as the massive Chinese market matures and other nations attempt to develop integrated solar supply chains.

Key Themes Covered in this Report:

- The impact of Chinese PV module oversupply on global solar energy markets

- Shifts in the global flat glass production base amid the European energy crisis

- Emerging growth opportunities in South and Southeast Asia

137 Tables & 89 Figures!

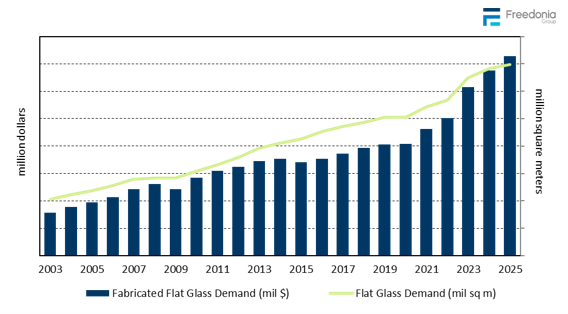

Global demand for flat glass is forecast to increase 2.8% per year to 16.0 billion square meters in 2030, valued at $194 billion. Gains will be driven by rising building construction and manufacturing activity, with production of solar modules continuing to represent the most dynamic growth segment.

Solar Energy Market to Diversify as Chinese Industry Matures

The global solar energy market for flat glass expanded dramatically between 2019 and 2025, increasing more than fivefold over this span. However, growth was concentrated in China, which is the world’s dominant manufacturer of PV modules. Oversupply in China’s module market posed additional challenges in 2023 into 2025, with intense price competition interrupting growth in PV module manufacturing in many countries.

Through 2030, growth in China’s solar energy market is expected to slow significantly, and non-China nations will account for an increased share of global flat glass sales gains. Global PV module manufacturing bases are expected to diversify, with the US and India particularly rising in importance as drivers of growth. However, the ongoing threat of oversupply issues in China – along with continued evolution of key regulatory supports – contributes to a volatile but dynamic environment.

Economic Development & Vertically Integrated Solar Supply Chain Boost Indian Market

India is expected to be the fastest growing national market for flat glass through 2030, well ahead of second-place Indonesia. In addition to gains associated with the solar energy market – where efforts to establish a vertically integrated solar supply chain will greatly boost PV module manufacturing – India is expected to post rapid advances in the architectural and motor vehicle markets. Growth will be fueled by broad economic development, with the middle class population expanding rapidly amid high levels of investment in commercial and industrial infrastructure.

Float Glass Production Capacity on the Rise in Developing Markets

Producers of float glass continue to invest heavily in new manufacturing capacity, with emerging markets in the Africa/Mideast and Asia/Pacific regions slated to bring a large number of new facilities on line in the second half of the 2020s. Strong growth prospects in these regions are attracting investment from a diverse array of sources, including major multinationals, local companies, and China-backed firms.

Global supply dynamics have been significantly impacted by the decline of West European float glass production, as the region shifted from a net exporter of flat glass in 2019 to the world’s largest net importer in 2025. Losses in West European output have not only created greater opportunities for less-developed markets to meet their needs domestically, but have also created the potential for the development of export industries to serve Western Europe from the Middle East and North Africa.

Global Flat Glass Report Details

Details about the Global Flat Glass Report

| Current Total Market Size |

14.0 billion square meters |

| Forecast Total Market Growth Rate |

2.8% CAGR from 2025-2030 |

| Historical Period |

2015-2025 |

| Forecast Period |

2025-2035 |

| Units Covered |

Square meters, metric tons, and US dollars |

| Regions |

North America, Central/South America, Western Europe, Eastern Europe, Asia/Pacific, Africa/Mideast |

| Countries Individually Covered |

Canada, Mexico, US, Brazil, France, Germany, Italy, Spain, UK, Poland, Russia, China, India, Indonesia, Japan, South Korea, Thailand, Vietnam, Iran, Turkey |

| Markets |

Architectural, motor vehicle, solar energy, other markets |

| Point Where Data is Measured |

Manufacturer’s Level |

| Additional Elements |

Market Share in Total and by Region, Near Term Trend Analysis, Mergers & Acquisitions, Float Glass Plant Capacities |

Leading Companies Driving Trends in the Global Flat Glass Industry

Leading companies in the Global Flat Glass Industry

| AGC |

KCC Glass |

| Cardinal Glass Industries |

NSG |

| Central Glass |

Saint-Gobain |

| CSG Holding |

Şişecam |

| Euroglas |

Taiwan Glass |

| Flat Glass Group |

Vitro |

| Fuyao Glass Industry Group |

Xinyi Glass |

| Guardian Industries |

Zhuzhou Kibing Group |

Historical Market Size & Growth Drivers

Flat glass is an essential component in a variety of industries, and demand tends to be closely tied to levels of activity in these industries. Historically, the most important demand drivers have been:

- building construction activity

- motor vehicle manufacturing and maintenance

- manufacturing of various types of durable goods, such as appliances, furniture, and consumer electronics

Use of flat glass in these applications tends to be mature, although industries may adjust their usage based on economic conditions. For example, builders may choose to emphasize designs with larger or smaller window areas based on the cost of glass relative to other materials. Regulatory factors – such as policies promoting the usage of multi-pane insulating glass units – can also influence demand trends.

Flat glass is also an important component of solar energy systems, which rose from a high-growth niche to one of the largest market segments during the first half of the 2020’s. This market tends to be particularly influenced by regulatory support in the form of subsidies and incentives, which contributes to a level of volatility.

The market for fabricated flat glass is also influenced by technological developments, which offer greater opportunities for sales growth in terms of value compared to basic, highly commoditized float glass. Value-added fabrication technologies include laminating, tempering, and coating, with the increasing emphasis on energy efficiency and environmental friendliness driving the adoption of these features.

Float glass is highly commoditized, and the costs of manufacturing these products are sensitive to the price of inputs like raw materials and energy. As a result, flat glass prices are heavily influenced by trends in the costs of these inputs.

Global Flat Glass Report Scope

This study analyzes the global market for flat glass by market and global region. Historical data (2015, 2019, and 2025) and forecasts for 2030 and 2035 are presented for fabricated flat glass demand in square meters and million dollars. In addition, production is presented in square meters and metric tons.

Flat glass demand is broken out by market:

- architectural, segmented into:

- residential

- nonresidential

- motor vehicle, segmented into:

- solar energy

- other markets, segmented into:

- appliances

- all other markets, such as electronic equipment, furniture, and other transportation equipment