Demand in unit terms is forecast to rise 2.2% annually to 1.1 billion units in 2028, supported by:

-

rising urbanization rates, as more housing is usually needed to accommodate mass urban-to-rural migration

-

increasing new housing construction, especially the replacement of informal dwellings with standard housing in developing countries

-

industrialization, infrastructure improvements, and growth in economic output, all of which impact business fixed investment and spending on nonresidential structures

-

the implementation of increasingly stringent building codes that promote the use of energy-efficient products and impact-resistant windows and doors

Energy Efficiency Remains Top of Mind for Many Window & Door Consumers

Increasing consumer awareness about the environmental effects of excessive energy usage means that energy efficient windows and doors are gaining significant traction. Products offering superior insulation (e.g., double or triple glazing, low-E glass, and insulated frames) are used to improve thermal performance, thereby reducing heating and cooling costs and lowering carbon footprints. These trends in consumer preferences have greatly benefited suppliers of vinyl and fiberglass windows and doors, which are generally more energy efficient than wood or metal iterations.

Growing Demand for Higher-Value, Impact-Resistant and Safety-Focused Products

Rising concerns over safety and security, especially in areas prone to extreme weather or crime, precipitate increased demand for impact-resistant windows and doors. These products are designed to withstand harsh conditions (such as hurricanes, tornadoes, and break-ins). In developed countries with high levels of severe weather activity, insurance requirements have led to increased usage based on rising disaster relief and insurance claim spending. Going forward, these products will contribute to greater increases in value demand because they command much higher average prices than standard window and door products.

Historical Market Trends & Growth Factors

Demand for windows and doors is impacted by several factors, including:

-

building construction activity

-

housing unit and nonresidential building sizes

-

improving housing quality and construction methods in developing areas

-

changes in energy efficiency regulations

-

shifts in regional aesthetic and performance preferences

-

growth in urbanization rates

-

natural disasters, particularly impacting demand for windows

Year-to-year volatility primarily tracks building construction activity. However, currency effects and major fluctuations in one particularly large market can have an outsized impact on global demand, the result of which is demand growth that can noticeably outperform or underperform the global building construction market.

Regional Trends

Production by Region

For the purposes of this study, window and door industry output in each country includes the value of imported components that are assembled locally into complete window and door units.

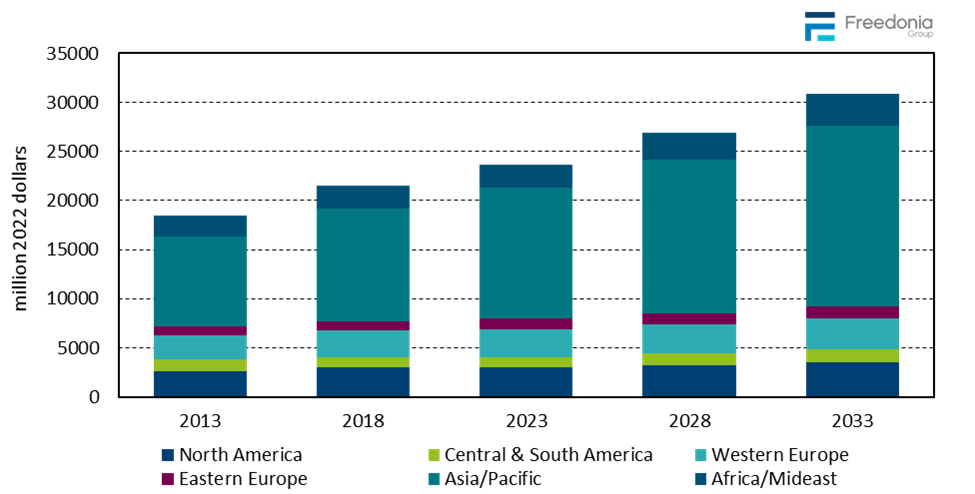

In general, window and door production in each market is close to total domestic demand. Interregional trade is generally limited by the high cost of transporting bulky windows and doors over long distances. Even in many of the most export-oriented fenestration product manufacturing countries – such as Canada and Germany – exports mainly travel only to neighboring countries. Consequently, the largest regional markets for windows and doors are also the largest regional producers of such products.

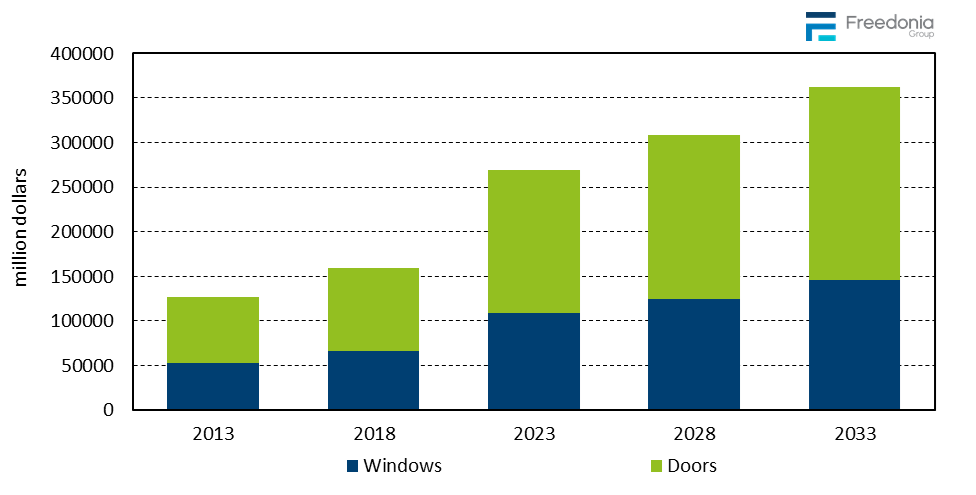

Through 2028, global window and door production is forecast to rise 2.8% per year to $308 billion:

-

The Asia/Pacific region will remain the leading producer of window and door products and a major exporter to all regions.

-

Production levels in Western Europe are projected to grow at a rate below the global average, largely due to market maturity.

However, Western Europe (along with North America) will remain the primary global source of high-end window and door products, particularly those produced in the US and Germany.

Product Overview

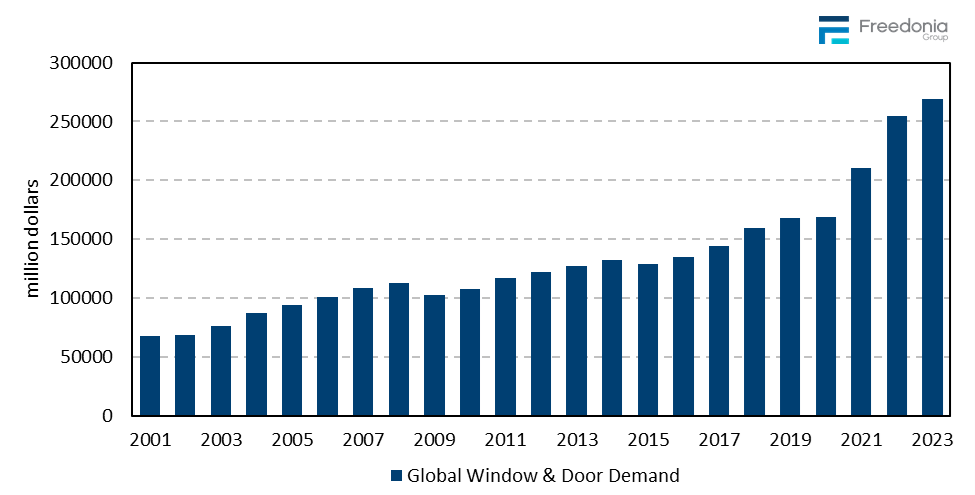

Global demand for windows and doors is forecast to rise 2.8% per year to $308 billion in 2028. Demand for windows will be supported by:

-

increasing demand for more energy-efficient building products

-

more stringent building codes throughout the world, such as those mandating impact-resistant products in coastal regions prone to severe weather (e.g., tropical cyclones)

-

rising interest in replacing older windows with more modern and easier opening iterations

-

increasing interest in large casement windows, skylights, roof windows, and curtain wall that let more light into structures while also imparting a unique appearance

Market advances in the doors segment will be driven by:

-

global rebounds in new housing construction, as far more doors are installed during the construction of a home than during most renovation projects

-

advances in nonresidential building construction in the Asia/Pacific region, supporting demand for metal nonresidential doors

-

global demand for safer and more secure structures, leading to demand for durable doors with enhanced security features

-

rising interest for doors with unique, customized, and modern designs that maximize natural light

Materials Overview

Demand by Material

Metal products account for the largest share of global window and door demand, bolstered by:

-

the common preference for steel windows and doors in nonresidential buildings, where durability, low maintenance requirements, and security are chief concerns

-

widespread use of metal (particularly low-cost aluminum) in developing countries, as durability is often prioritized more heavily than energy efficiency and aesthetics in those markets

However, producers of metal windows and doors will continue to face competition from vinyl products; the latter can offer better energy efficiency at competitive prices, in addition to good aesthetics.

The wood segment will continue to be buoyed by the large interior door market, where wood remains the preferred material. However, suppliers of other materials are continuing to place increasing pressure on wood window and door manufacturers by producing products that mimic the aesthetics of wood. Nevertheless, historical preferences for wood architectural elements will continue to drive sales in many countries.

Materials Comparison

Each of the materials used for windows and doors has advantages and disadvantages that influence builders and building owners when they make purchasing decisions. While price is a foremost consideration, certain advantages – such as long lifespan and improved energy efficiency – can outweigh the burden of high initial costs.

It is important to note that the capabilities of products within the same material category vary widely depending on how well they are manufactured. For instance, wood- and metal-frame windows can be designed to achieve energy efficiency levels that surpass those of some plastic products. Likewise, there are highly durable vinyl windows and doors that meet the same impact resistance requirements as metal products.

Building Construction Outlook

Building construction plays a critical role in shaping demand for windows and doors, as these elements are essential components in any structure. The overall volume of construction activity, including both new builds and renovations, directly influences the quantity of the windows and doors required.

Additionally, the types and sizes of buildings being constructed impact the specific kinds of windows and doors in demand. Residential homes often favor traditional or energy-efficient windows and doors, while commercial or industrial buildings tend to require larger and/or more specialized units designed for durability or safety. The variation in building types ensures that a diverse range of window and door products are needed to meet specific structural and aesthetic requirements.

Global building construction activity is forecast to increase 2.5% annually through 2028, led by healthy growth in the Asia/Pacific region. Gains will be more restrained in North America, and in particular Western Europe, where building construction expenditures are only forecast to grow at an annual rate of less than 1.0% through 2028. High interest rates, falling building permit demand, geopolitical instability, and rising housing prices will inhibit stronger growth in Western Europe.

Report Details

This study examines the global window and door market by product, material, market, and geographic region in value terms at the manufacturers’ level (i.e., excluding the value of features and services added between the manufacturer and end user, including door hanging and finishing operations not offered by the door slab manufacturer). Total unit demand is also provided at the global, regional, subregional, and country level. Historical data for 2013, 2018, and 2023, and forecasts for 2028 and 2033 are provided in US nominal dollars. Additionally, annual data from 2020 to 2027 is also provided.

For the purposes of this study, the value of installed glazing is included in the demand numbers for all window products. Windows with multiple openings (e.g., bay and bow types) that are sold as one unit are one window.

For doors, the value of installed glazing, sidelites, and/or transoms is included if these features are sold by the manufacturer as part of the framed system.

Major window products included in the study are:

-

single- and double-hung windows

-

casement windows

-

sliding and swing windows

-

architectural and stationary windows

Major door products include the following types:

-

interior – including panel (e.g., stile-and-rail, and French), flush, and molded

-

entry (manually opened)

-

sliding patio (including multi-slide types)

-

swinging patio (including multifold types)

-

residential garage

-

automated sliding and swinging

-

overhead (including sectional and rolling steel and high-speed plastic roll-up types)

-

storm

To avoid double counting, parts and components sold to, or imported by, manufacturers for assembly into new windows and doors are excluded from the scope of this study.

Also excluded are:

Separately sold replacement hardware not typically sold as part of the window or door unit (e.g., door knobs, locks, door stops, and garage door openers) are outside the scope of this study. However, the value of these products is included when they are sold as part of an integrated new window or door unit.

Window and door demand is segmented by the following framing materials:

Engineered wood products include those manufactured from particleboard, plywood, medium density fiberboard (MDF), and laminated veneer lumber (LVL).

The wood segment includes wood doors clad with metal or plastic materials but that have a wood interior. Wood windows include only those products in which all the framing components (e.g., jambs, sills, stiles, rails, and mullions) are made of wood.

Window and door demand is also segmented into the following markets:

-

new residential buildings

-

residential building improvement and repair

-

new nonresidential buildings

-

nonresidential building improvement and repair

The new residential and nonresidential markets include only those products installed in the construction of new residential and nonresidential structures. Improvement and repair markets encompass windows, doors, and related components sold to replace or repair existing products, or as part of a remodeling, renovation, or expansion project.

Excluded from the definition of residential buildings are housing units located in a structure whose primary purpose is something other than habitation. Thus, a small living space contained in a larger retail facility would be classified as part of a retail building and not a residential building.