Report Overview

Featuring 96 tables and 49 figures – available in Excel and Powerpoint! Learn More

This study examines the US market for plastic food packaging, defined as primary and secondary packaging materials sold to food manufacturers, primarily for  products targeted at retail or foodservice markets. Historical data are provided for 2012, 2017, and 2022, with forecasts through 2027 and 2032. Annual data is provided for 2018-2026. Data are provided in current dollar value. Also provided is an analysis of key industry players.

products targeted at retail or foodservice markets. Historical data are provided for 2012, 2017, and 2022, with forecasts through 2027 and 2032. Annual data is provided for 2018-2026. Data are provided in current dollar value. Also provided is an analysis of key industry players.

See our discussion regarding Plastic Food Packaging

Demand for food packaging made from plastic is forecast to increase 3.0% per year to $36 billion in 2027. Plastic will continue to be the largest and fastest growing of the major food packaging materials – thanks to its versatile nature, low cost, and excellent performance – although other, more sustainable materials like molded fiber will provide increasing competition going forward.

Sustainability Will Have Nuanced Effects on Plastic Packaging

The growing impact of sustainability on the packaging market will affect plastic in several distinct ways. Despite plastic being the leading target for sustainability conversions, end users continue to value plastic over other materials based on cost and performance. However, manufacturers have employed several techniques to improve the environmental profile of their products in recent years, including:

-

incorporating greater amounts of recycled content

-

ensuring their plastic packaging is recyclable, with a trend toward monomaterial packaging becoming more prevalent

-

light weighting and source reduction

Additionally, bioplastics will play a more significant role in the plastic food packaging market going forward. However, bioplastics must overcome price and scalability issues in order to become truly competitive with conventional plastics.

Flexible Packaging Will Continue to Gain Favor Among End Users

Demand for flexible plastic food packaging will be supported by both its performance benefits and favorable environmental profile compared to rigid packaging. Flexible plastic packaging is highly versatile, conforming to various product shapes, sizes, and applications, allowing for widespread market penetration. Moreover, it often requires fewer resources to manufacture and produces less waste.

Gains will also be driven by the increasing popularity of stand-up pouches, which are valued for their aesthetics and portability. Additionally, newer flexible packaging products, such as vacuum skin packaging and brick packs in meat packaging and bag-in-box formats (which use plastic bladders) for foodservice and retail, will support demand growth.

Healthy Growth in Prepared Foods and Candy & Confections Will Support Demand

While meat, poultry, and seafood will continue to account for most of plastic’s absolute gains, faster growing markets such as prepared foods and candy and confections will support even greater demand for plastic food packaging overall, driven by:

-

expanding availability of fresh/refrigerated prepared foods like grab-and-go complete meals, salads, and sandwiches at grocery and convenience stores

-

increasing sales of pre-packaged refrigerated meals (including prepared meats and pasta dishes) from leading food companies

-

the trend toward smaller individually wrapped versions of larger candies

- shift to higher-value packaging formats such as stand-up pouches and two-piece containers

Historical Market Trends

Shifts in demand for plastic food packaging from year to year are determined by a few factors, primarily related to the production and marketing of food products. These activities in turn are influenced by:

-

demographic trends such as age, average household size, and levels of disposable income

-

consumer spending on food and the balance between at-home and away-from-home meals

-

food preferences (e.g., demand for enhanced convenience or for organic products)

-

restaurant and other foodservice industry revenues

In addition, several competitive variables determine the mix of packaging types used and their cost, including:

-

raw material and conversion costs

-

changes in the mix of foods being packaged, particularly in terms of food format (canned, dried, frozen, fresh)

-

trends in packaging size and format, such as shifts toward smaller single-serving packages, family size units, or multipacks

-

the proportion of food that is sold via retail channels versus foodservice establishments

-

environmental and regulatory factors, including trends such as source reduction, the use of recycled content, and recyclability

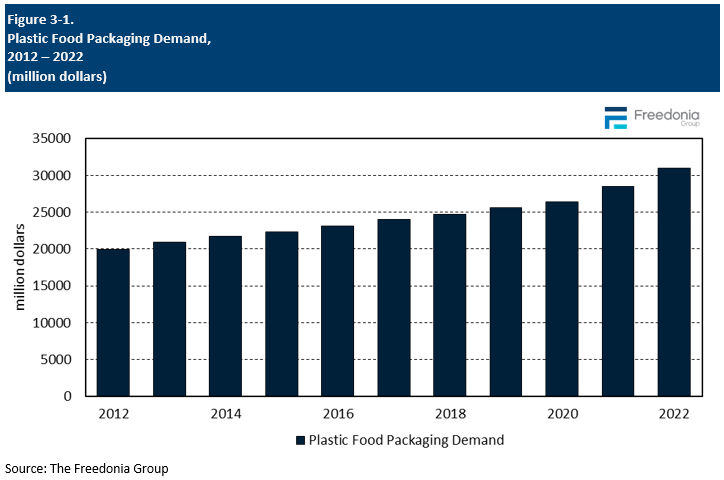

Plastic food packaging demand growth in 2021 and 2022 experienced a strong acceleration in value terms compared to previous years due to the significant inflation following supply chain issues caused by the 2020 pandemic.

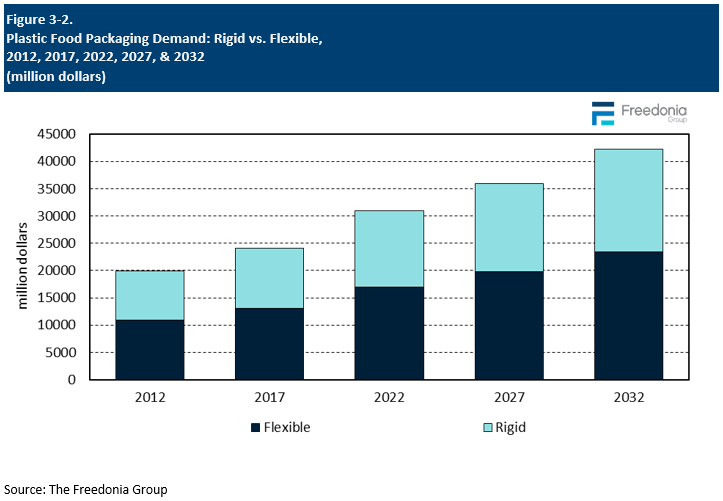

Demand by Packaging Format (Rigid vs. Flexible)

In the broadest terms, food packaging includes rigid and flexible products, with competition coming both between these two broad types and among the products within each of those categories. Factors that determine the mix of packaging at this level include cost and product performance, though sustainability initiatives are increasingly important.

Demand for plastic food packaging overall is forecast to rise 3.0% per year to $35.9 billion in 2027. In addition to overall growth in food production, the mix of foods produced, and trends in packaging end uses, other factors specifically driving growth in plastic packaging usage include:

-

sustainability initiatives, which promotes demand for plastic packaging seen as more environmentally friendly, such as bioplastics, which are more expensive than traditional products

-

the popularity of single-serving and snack sizes, which are more intensive users of packaging (in terms of packaging cost per volume of food produced)

-

the need for food product differentiation, which drives demand for higher priced packaging with value-added features or improved shelf-appeal

-

recent inflationary pressures, with some manufacturers taking to utilizing “shrinkflation” to cut costs rather than increase prices, increasing unit demand for these products

-

a general move toward higher-value packaging due to performance improvements, such as increasing shelf life or reducing leakage

-

the continued penetration of aseptic processing over more traditional processing methods, which elicits the need for certain higher-value packaging formats such as pouches and bag-in-box

Pricing Trends

Pricing is an important factor in selecting packaging for a particular food application. Price competition in the industry is intense, due to the prevalence of relatively low-technology, commodity-type products.

The cost of raw materials, such as plastic resins and petroleum, is the primary determinant of pricing for plastic food packaging, as they typically represent at least half of the final packaging price.

Other key factors influencing the price of plastic food packaging include:

-

the degree of lightweighting and downsizing activity – efforts that cut costs per unit by reducing the packaging size either through using lighter-weight packaging or marginally decreasing product volume

-

the presence of value-added features such as spouts and reclosable zippers

-

the packaging product mix, both in terms of package size and plastic composition

-

supply chain pressures that squeeze packaging producers between large raw material suppliers on one end and large food processors on the other, leaving them less options for pricing flexibility

-

pressure to improve sustainability, which can result in the use of higher cost materials such as bioplastics

In 2021, the price of raw material inputs used in the production of plastic food packaging increased dramatically due to shortages caused by supply chain issues, leading to a large increase in end pricing of food packaging products. These price increases continued through most of 2022, before mostly flattening in 2023. Bioplastics were less affected as their growing economies of scale helped offset the impact of increased raw material inputs.

Going forward, plastic packaging pricing is expected to normalize and is forecast to see price growth in line with historical trends beginning in 2024.

Sustainability in Packaging

While environmental concerns have impacted the choice of packaging in the food industry to some degree for decades, sustainability has recently become one of the most important trends in the global manufacturing industry. Plastic packaging is a high-profile target for those looking for sustainability improvements because it is:

-

used pervasively by most industries worldwide

-

is generally meant to be disposable

-

often finds its way into the environment

However, the pursuit of sustainability is not straightforward, as packaging must also continue to provide acceptable performance, especially in the food industry where it plays a key role in maintaining food quality and safety. In addition, for foods to remain affordable and food companies to remain profitable, packaging costs will remain a key variable in packaging choice.

To understand whether a specific type of packaging is truly sustainable, other factors must also be considered beyond the renewable nature of its raw materials and the final packaging’s levels of recyclability or compostability. These factors include:

At present, there is no one perfect packaging choice for all applications. Most packaging materials currently on the market have advantages and disadvantages, and even newer products are being introduced primarily for their sustainability merits. Packaging end users must choose the product that provides the best balance of cost, performance, and environmental impact and then find a way to help customers understand the benefits of that packaging choice.